In econometrics, the autoregressive conditional heteroskedasticity (ARCH) model is a statistical model for time series data that describes the variance...

23 KB (3,820 words) - 19:30, 26 May 2024

In the statistical analysis of time series, autoregressive–moving-average (ARMA) models are a way to describe of a (weakly) stationary stochastic process...

19 KB (2,445 words) - 16:29, 1 October 2024

In statistics, econometrics, and signal processing, an autoregressive (AR) model is a representation of a type of random process; as such, it can be used...

34 KB (5,421 words) - 21:34, 14 November 2024

variances are important parts of autoregressive conditional heteroskedasticity (ARCH) models. The conditional variance of a random variable Y given another...

6 KB (1,099 words) - 10:03, 4 June 2024

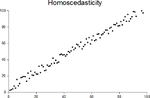

Homoscedasticity and heteroscedasticity (redirect from Heteroskedasticity)

White, Halbert (1980). "A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity". Econometrica. 48 (4): 817–838...

27 KB (3,191 words) - 23:32, 30 August 2024

role in data analysis aimed at identifying the extent of the lag in an autoregressive (AR) model. The use of this function was introduced as part of the Box–Jenkins...

9 KB (1,129 words) - 10:23, 1 August 2024

Vector autoregression (redirect from Vector autoregressive model)

process model. VAR models generalize the single-variable (univariate) autoregressive model by allowing for multivariate time series. VAR models are often...

22 KB (3,524 words) - 01:03, 22 November 2024

changes of variance over time (heteroskedasticity). These models represent autoregressive conditional heteroskedasticity (ARCH) and the collection comprises...

41 KB (4,874 words) - 20:48, 23 November 2024

of Finance, May 1982 V. 37: #2 1982 – Robert Engle, Autoregressive Conditional Heteroskedasticity With Estimates of the Variance of U.K. Inflation, Seminal...

32 KB (3,659 words) - 16:49, 13 October 2024

elements of the matrix are equal to each other. On the other hand, an autoregressive matrix is often used when variables represent a time series, since correlations...

38 KB (5,347 words) - 03:08, 25 November 2024

Logistic regression (redirect from Conditional logit analysis)

be to predict the likelihood of a homeowner defaulting on a mortgage. Conditional random fields, an extension of logistic regression to sequential data...

127 KB (20,643 words) - 21:34, 15 October 2024

Granger causality analysis is usually performed by fitting a vector autoregressive model (VAR) to the time series. In particular, let X ( t ) ∈ R d × 1...

26 KB (3,372 words) - 16:18, 15 November 2024

via scatterplots Quantitative measures of dependence Descriptions of conditional distributions The main reason for differentiating univariate and bivariate...

8 KB (961 words) - 01:30, 17 October 2024

is no linear relationship. The partial correlation coincides with the conditional correlation if the random variables are jointly distributed as the multivariate...

22 KB (3,475 words) - 02:04, 27 October 2024

Cross-correlation (XCF) ARMA model ARIMA model (Box–Jenkins) Autoregressive conditional heteroskedasticity (ARCH) Vector autoregression (VAR) Frequency domain...

20 KB (3,012 words) - 03:53, 9 November 2024

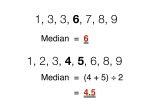

Median (section Conditional median)

{\displaystyle t\mapsto F_{X|Y=y}^{-1}(t)} is the inverse of the conditional cdf (i.e., conditional quantile function) of x ↦ F X | Y ( x | y ) {\displaystyle...

62 KB (7,974 words) - 14:03, 22 November 2024

ISBN 9780412039911. Park SY, Bera AK (2009). "Maximum entropy autoregressive conditional heteroskedasticity model". J. Econom. 150 (2): 219–230. doi:10.1016/j.jeconom...

55 KB (6,339 words) - 04:56, 14 November 2024

Cross-correlation (XCF) ARMA model ARIMA model (Box–Jenkins) Autoregressive conditional heteroskedasticity (ARCH) Vector autoregression (VAR) Frequency domain...

29 KB (3,152 words) - 22:26, 4 October 2024

in Missouri, Illinois, and the surrounding regions Autoregressive conditional heteroskedasticity, a time series regression model of the standard deviation...

4 KB (485 words) - 09:59, 18 June 2024

(X_{1}\mid X_{2}=x_{2})=1-\rho ^{2};} thus the conditional variance does not depend on x2. The conditional expectation of X1 given that X2 is smaller/bigger...

65 KB (9,519 words) - 21:04, 16 November 2024

variables contained in high-dimensional contingency tables. If some of the conditional independences are revealed, then even the storage of the data can be...

15 KB (1,945 words) - 20:16, 30 October 2023

introduced the technique in 1983, defining the propensity score as the conditional probability of a unit (e.g., person, classroom, school) being assigned...

19 KB (2,470 words) - 02:11, 30 September 2024

S2CID 2884450. McQuarrie, A. D. R.; Tsai, C.-L. (1998). Regression and Time Series Model Selection. World Scientific. Sparse Vector Autoregressive Modeling...

11 KB (1,673 words) - 18:18, 11 November 2024

Cross-correlation (XCF) ARMA model ARIMA model (Box–Jenkins) Autoregressive conditional heteroskedasticity (ARCH) Vector autoregression (VAR) Frequency domain...

21 KB (3,066 words) - 15:00, 17 June 2024

Park, Sung Y.; Bera, Anil K. (2009). "Maximum entropy autoregressive conditional heteroskedasticity model" (PDF). Journal of Econometrics. 150 (2): 219–230...

81 KB (11,922 words) - 05:02, 25 November 2024

Correlogram Autocovariance Autoregressive conditional duration Autoregressive conditional heteroskedasticity Autoregressive fractionally integrated moving...

87 KB (8,285 words) - 04:29, 7 October 2024

moving average (EWMA). Technically it can also be classified as an autoregressive integrated moving average (ARIMA) (0,1,1) model with no constant term...

27 KB (4,340 words) - 13:29, 23 November 2024

subpopulations defined by X = 1 and X = 0 are defined in terms of the conditional probabilities given X, i.e., P(Y |X): Y = 1 Y = 0 X = 1 p 11 p 11 + p...

49 KB (7,072 words) - 06:11, 16 October 2024

{\displaystyle \beta _{j}} . An example of a linear time series model is an autoregressive moving average model. Here the model for values { X t {\displaystyle...

5 KB (831 words) - 23:29, 17 November 2024

financial market volatility and for the GARCH (generalized autoregressive conditional heteroskedasticity) model. Tim Bollerslev received his MSc in economics...

5 KB (392 words) - 09:32, 10 November 2024