In econometrics, the autoregressive conditional heteroskedasticity (ARCH) model is a statistical model for time series data that describes the variance...

23 KB (3,837 words) - 12:33, 15 January 2025

In statistics, econometrics, and signal processing, an autoregressive (AR) model is a representation of a type of random process; as such, it can be used...

34 KB (5,421 words) - 03:27, 4 February 2025

variances are important parts of autoregressive conditional heteroskedasticity (ARCH) models. The conditional variance of a random variable Y given another...

6 KB (1,099 words) - 10:03, 4 June 2024

In the statistical analysis of time series, autoregressive–moving-average (ARMA) models are a way to describe a (weakly) stationary stochastic process...

19 KB (2,444 words) - 14:29, 6 January 2025

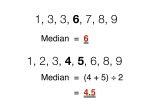

Median (section Conditional median)

{\displaystyle t\mapsto F_{X|Y=y}^{-1}(t)} is the inverse of the conditional cdf (i.e., conditional quantile function) of x ↦ F X | Y ( x | y ) {\displaystyle...

62 KB (7,974 words) - 14:03, 22 November 2024

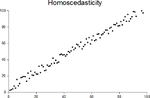

Homoscedasticity and heteroscedasticity (redirect from Heteroskedasticity)

White, Halbert (1980). "A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity". Econometrica. 48 (4): 817–838...

27 KB (3,191 words) - 23:32, 30 August 2024

Likelihood function (redirect from Conditional likelihood)

interpreted within the context of information theory. Bayes factor Conditional entropy Conditional probability Empirical likelihood Likelihood principle Likelihood-ratio...

64 KB (8,545 words) - 07:33, 5 February 2025

Continuous uniform distribution (section Example 2. Using the continuous uniform distribution function (conditional))

Park, Sung Y.; Bera, Anil K. (2009). "Maximum entropy autoregressive conditional heteroskedasticity model". Journal of Econometrics. 150 (2): 219–230. CiteSeerX 10...

27 KB (4,219 words) - 07:31, 30 October 2024

Correlogram Autocovariance Autoregressive conditional duration Autoregressive conditional heteroskedasticity Autoregressive fractionally integrated moving...

87 KB (8,285 words) - 04:29, 7 October 2024

changes of variance over time (heteroskedasticity). These models represent autoregressive conditional heteroskedasticity (ARCH) and the collection comprises...

42 KB (5,010 words) - 01:42, 14 January 2025

role in data analysis aimed at identifying the extent of the lag in an autoregressive (AR) model. The use of this function was introduced as part of the Box–Jenkins...

9 KB (1,129 words) - 10:23, 1 August 2024

Park, Sung Y.; Bera, Anil K. (2009). "Maximum entropy autoregressive conditional heteroskedasticity model" (PDF). Journal of Econometrics. 150 (2). Elsevier:...

43 KB (6,632 words) - 16:39, 13 February 2025

Vector autoregression (redirect from Vector autoregressive model)

process model. VAR models generalize the single-variable (univariate) autoregressive model by allowing for multivariate time series. VAR models are often...

22 KB (3,542 words) - 03:58, 20 January 2025

{Var} [X\mid Y])+\operatorname {Var} (\operatorname {E} [X\mid Y]).} The conditional expectation E ( X ∣ Y ) {\displaystyle \operatorname {E} (X\mid Y)}...

59 KB (10,189 words) - 21:12, 3 February 2025

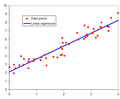

as one of the parameters. As another example, consider a first-order autoregressive model, defined by xi = c + φxi−1 + εi, with the εi being i.i.d. Gaussian...

42 KB (5,483 words) - 14:30, 15 February 2025

ISBN 9780412039911. Park SY, Bera AK (2009). "Maximum entropy autoregressive conditional heteroskedasticity model". Journal of Econometrics. 150 (2): 219–230. doi:10...

55 KB (6,358 words) - 19:28, 27 January 2025

Park, Sung Y.; Bera, Anil K. (2009). "Maximum entropy autoregressive conditional heteroskedasticity model" (PDF). Journal of Econometrics. 150 (2): 219–230...

83 KB (12,195 words) - 14:40, 12 February 2025

Cross-correlation (XCF) ARMA model ARIMA model (Box–Jenkins) Autoregressive conditional heteroskedasticity (ARCH) Vector autoregression (VAR) Frequency domain...

115 KB (14,450 words) - 19:54, 13 February 2025

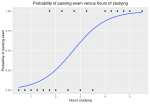

Logistic regression (redirect from Conditional logit analysis)

be to predict the likelihood of a homeowner defaulting on a mortgage. Conditional random fields, an extension of logistic regression to sequential data...

127 KB (20,641 words) - 16:46, 9 February 2025

subpopulations defined by X = 1 and X = 0 are defined in terms of the conditional probabilities given X, i.e., P(Y |X): Y = 1 Y = 0 X = 1 p 11 p 11 + p...

49 KB (7,072 words) - 06:11, 16 October 2024

commonly, the conditional median or some other quantile is used. Like all forms of regression analysis, linear regression focuses on the conditional probability...

75 KB (10,428 words) - 07:51, 10 February 2025

Cross-correlation (XCF) ARMA model ARIMA model (Box–Jenkins) Autoregressive conditional heteroskedasticity (ARCH) Vector autoregression (VAR) Frequency domain...

22 KB (2,430 words) - 11:52, 1 February 2025

standard deviation of a slice of the multivariate distribution (i.e. the conditional distribution) along the line in the direction of the unit vector η ^...

59 KB (8,181 words) - 00:45, 1 February 2025

(X_{1}\mid X_{2}=x_{2})=1-\rho ^{2};} thus the conditional variance does not depend on x2. The conditional expectation of X1 given that X2 is smaller/bigger...

66 KB (9,655 words) - 09:14, 16 February 2025

Granger causality analysis is usually performed by fitting a vector autoregressive model (VAR) to the time series. In particular, let X ( t ) ∈ R d × 1...

26 KB (3,375 words) - 05:33, 26 January 2025

elements of the matrix are equal to each other. On the other hand, an autoregressive matrix is often used when variables represent a time series, since correlations...

39 KB (5,358 words) - 18:05, 29 January 2025

(2003). "Time-series econometrics: Cointegration and autoregressive conditional heteroskedasticity". Advanced Information on the Bank of Sweden Prize in...

15 KB (2,171 words) - 15:26, 17 August 2024

Park, Sung Y.; Bera, Anil K. (2009). "Maximum entropy autoregressive conditional heteroskedasticity model" (PDF). Journal of Econometrics. 150 (2): 219–230...

66 KB (9,067 words) - 16:28, 14 February 2025

(see linear regression), this allows the researcher to estimate the conditional expectation (or population average value) of the dependent variable when...

38 KB (5,289 words) - 14:49, 15 February 2025

Cross-correlation (XCF) ARMA model ARIMA model (Box–Jenkins) Autoregressive conditional heteroskedasticity (ARCH) Vector autoregression (VAR) Frequency domain...

91 KB (10,677 words) - 18:17, 14 February 2025