Itô calculus, named after Kiyosi Itô, extends the methods of calculus to stochastic processes such as Brownian motion (see Wiener process). It has important...

31 KB (4,554 words) - 03:50, 6 May 2025

from the original on 30 October 2008. Itô calculus Itô diffusion Itô integral Itô–Nisio theorem Itô isometry Itô's lemma Black–Scholes model O'Connor, John...

19 KB (1,702 words) - 21:56, 18 June 2025

flavours of stochastic calculus are the Itô calculus and its variational relative the Malliavin calculus. For technical reasons the Itô integral is the most...

5 KB (620 words) - 23:30, 1 July 2025

In mathematics, Itô's lemma or Itô's formula (also called the Itô–Döblin formula) is an identity used in Itô calculus to find the differential of a time-dependent...

28 KB (5,921 words) - 04:54, 12 May 2025

Stratonovich integral (redirect from Stratonovich stochastic calculus)

is a stochastic integral, the most common alternative to the Itô integral. Although the Itô integral is the usual choice in applied mathematics, the Stratonovich...

10 KB (1,777 words) - 13:55, 1 July 2025

definition was first proposed by Kiyosi Itô in the 1940s, leading to what is known today as the Itô calculus. Another construction was later proposed...

36 KB (5,634 words) - 11:32, 24 June 2025

In Itô calculus, the Euler–Maruyama method (also simply called the Euler method) is a method for the approximate numerical solution of a stochastic differential...

10 KB (1,596 words) - 01:17, 9 May 2025

deals with extremizing functionals Itô calculus An extension of calculus to stochastic processes. Logical calculus, a formal system that defines a language...

5 KB (657 words) - 10:42, 11 July 2025

called a hepatic stellate cell Ito-toren, an office building in Amsterdam Itô calculus Itô's lemma, used in stochastic calculus Itoh–Tsujii inversion algorithm...

2 KB (306 words) - 14:11, 28 October 2024

known for his contributions to local volatility modeling and Functional Itô Calculus. He is also an Instructor at New York University since 2005, in the Courant...

5 KB (476 words) - 20:45, 3 August 2024

given mean return. Thus, although the language of finance now involves Itô calculus, management of risk in a quantifiable manner underlies much of the modern...

34 KB (3,956 words) - 20:32, 27 May 2025

be understood in the Itô sense. Thus this provides a method of extending the Itô integral to non adapted integrands. The calculus allows integration by...

16 KB (2,660 words) - 04:25, 5 July 2025

Walter; Tschiderer, Bertram (21 November 2018). "Applying Itô calculus to Otto calculus" (PDF). Otto, Felix (2001-01-31). "The geometry of dissipative...

3 KB (214 words) - 22:52, 26 May 2025

f}{\partial t}}.} Stochastic differential equation Itô calculus Fokker–Planck equation Markov process Diffusion Itô diffusion Jump diffusion Sample-continuous...

5 KB (1,099 words) - 13:27, 10 July 2025

Sample-continuous process Stationary process Stochastic calculus Itô calculus Malliavin calculus Semimartingale Stratonovich integral Stochastic control...

5 KB (407 words) - 21:21, 25 August 2023

In mathematics, the Itô isometry, named after Kiyoshi Itô, is a crucial fact about Itô stochastic integrals. One of its main applications is to enable...

11 KB (1,824 words) - 02:29, 13 May 2025

Integral (redirect from Integral calculus)

of computing an integral, is one of the two fundamental operations of calculus, the other being differentiation. Integration was initially used to solve...

69 KB (9,288 words) - 03:06, 30 June 2025

differential and integral calculus is not applicable to such processes. In the 1940s Kiyoshi Itō developed a stochastic calculus (the Ito calculus) for such random...

12 KB (1,339 words) - 07:05, 16 June 2025

Itô QSDE, it is necessary to know something about the bath statistics.: 159 In the context of the white noise formalism described earlier, the Itô QSDE...

19 KB (3,148 words) - 15:01, 12 February 2025

x_{n}} . Hilbert spaces are also used throughout the foundations of the Itô calculus. To any square-integrable martingale, it is possible to associate a Hilbert...

128 KB (17,469 words) - 11:09, 10 July 2025

compounding in pricing these instruments is a natural consequence of Itô calculus, where financial derivatives are valued at ever-increasing frequency...

21 KB (2,890 words) - 06:24, 14 July 2025

is limited to two dimensions Inversive ring geometry Itô calculus extends the methods of calculus to stochastic processes such as Brownian motion (see...

71 KB (7,692 words) - 16:40, 4 July 2025

{\displaystyle \mathrm {d} X_{t}^{j}} " can be defined in the sense of Itô. However, Itô's calculus is defined in the sense of L 2 {\displaystyle L^{2}} and is in...

29 KB (5,685 words) - 18:42, 14 June 2025

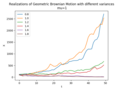

Geometric Brownian motion (category Non-Newtonian calculus)

^{2}}{2}}\right)t+\sigma W_{t}\right).} The derivation requires the use of Itô calculus. Applying Itô's formula leads to d ( ln S t ) = ( ln S t ) ′ d S t + 1 2...

14 KB (2,140 words) - 02:45, 6 May 2025

-r}{\sigma }}} is known as the market price of risk. Utilizing rules within Itô calculus, one may informally differentiate with respect to t {\displaystyle t}...

16 KB (2,684 words) - 04:31, 23 April 2025

Rama Cont (section Causal functional calculus)

Lucia; Cont, Rama (2016). Stochastic Integration by Parts and Functional Itô Calculus. Advanced Courses in Mathematics - CRM Barcelona. doi:10.1007/978-3-319-27128-6...

24 KB (2,041 words) - 05:17, 30 June 2025

Skorokhod's embedding theorem Stationary process Stochastic calculus Itô calculus Malliavin calculus Stratonovich integral Time series analysis Autoregressive...

11 KB (1,000 words) - 14:07, 2 May 2024

Kushner–Stratonovich) equation. However, the correct equation in terms of Itō calculus was first derived by Kushner although a more heuristic Stratonovich version...

4 KB (800 words) - 22:17, 23 August 2024

Skorokhod integral (category Stochastic calculus)

Japan-USSR Symp. Probab. Th.2.: 111–114. Kuo, Hui-Hsiung (2014). "The Itô calculus and white noise theory: a brief survey toward general stochastic integration"...

8 KB (1,427 words) - 02:51, 15 March 2024

D. (1987). Diffusions, Markov Processes and Martingales. Vol. II, Itô, Calculus. Cambridge University Press. p. 50. doi:10.1017/CBO9780511805141. ISBN 0-521-77593-0...

2 KB (188 words) - 06:34, 14 April 2025