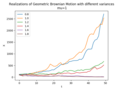

A stochastic differential equation (SDE) is a differential equation in which one or more of the terms is a stochastic process, resulting in a solution...

36 KB (5,616 words) - 15:19, 12 July 2024

Stochastic partial differential equations (SPDEs) generalize partial differential equations via random force terms and coefficients, in the same way ordinary...

8 KB (826 words) - 03:40, 5 July 2024

A backward stochastic differential equation (BSDE) is a stochastic differential equation with a terminal condition in which the solution is required to...

5 KB (613 words) - 01:49, 18 November 2024

partial differential equations (PDEs) which may be with respect to more than one independent variable, and, less commonly, in contrast with stochastic differential...

44 KB (5,222 words) - 16:18, 1 November 2024

In mathematics, a differential equation is an equation that relates one or more unknown functions and their derivatives. In applications, the functions...

29 KB (3,628 words) - 15:16, 20 August 2024

dynamical system and differential equation topics, by Wikipedia page. See also list of partial differential equation topics, list of equations. Deterministic...

5 KB (413 words) - 21:49, 5 November 2024

In physics, a Langevin equation (named after Paul Langevin) is a stochastic differential equation describing how a system evolves when subjected to a combination...

30 KB (5,246 words) - 19:53, 25 November 2024

Tsirelson's stochastic differential equation (also Tsirelson's drift or Tsirelson's equation) is a stochastic differential equation which has a weak solution...

4 KB (687 words) - 11:13, 21 July 2024

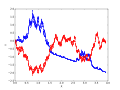

with drift. It is an important example of stochastic processes satisfying a stochastic differential equation (SDE); in particular, it is used in mathematical...

14 KB (2,237 words) - 23:19, 21 November 2024

In mathematics, stochastic analysis on manifolds or stochastic differential geometry is the study of stochastic analysis over smooth manifolds. It is...

20 KB (3,647 words) - 00:21, 17 May 2024

Itô calculus (redirect from Ito stochastic calculus)

stochastic processes such as Brownian motion (see Wiener process). It has important applications in mathematical finance and stochastic differential equations...

30 KB (4,486 words) - 14:14, 26 August 2024

multifractals in turbulence, the stochastic differential equation for growth models for random aggregation (the Kardar–Parisi–Zhang equation) and his groundbreaking...

23 KB (1,961 words) - 22:09, 17 September 2024

In mathematics, a partial differential equation (PDE) is an equation which computes a function between various partial derivatives of a multivariable function...

51 KB (7,288 words) - 03:57, 24 November 2024

random variable Yt : Ω → Rn given by the solution to an Itō stochastic differential equation of the form d Y t = b ( t , Y t ) d t + σ ( t , Y t ) d B t...

13 KB (2,142 words) - 20:36, 4 July 2024

can be generalized to stochastic systems, in which case the HJB equation is a second-order elliptic partial differential equation. A major drawback, however...

14 KB (2,050 words) - 17:50, 26 April 2024

papers developing the field of stochastic calculus, which involves stochastic integrals and stochastic differential equations based on the Wiener or Brownian...

166 KB (18,416 words) - 04:16, 13 November 2024

of assets—are stochastic. Backward stochastic differential equation Stochastic process Control theory Multiplier uncertainty Stochastic scheduling Definition...

12 KB (1,683 words) - 09:57, 3 March 2023

convection–diffusion equation is a parabolic partial differential equation that combines the diffusion and convection (advection) equations. It describes physical...

20 KB (2,733 words) - 16:04, 5 November 2024

stochastic differential equations (QSDE) that are analogous to classical Langevin equations. For the remainder of this article stochastic calculus will...

19 KB (3,218 words) - 23:03, 3 October 2022

adjoint of the infinitesimal generator of the underlying stochastic process. The Klein–Kramers equation is a special case of that. For a Feller process ( X...

9 KB (1,720 words) - 21:39, 25 November 2024

Ornstein–Uhlenbeck process (category Stochastic differential equations)

process x t {\displaystyle x_{t}} is defined by the following stochastic differential equation: d x t = − θ x t d t + σ d W t {\displaystyle dx_{t}=-\theta...

30 KB (4,605 words) - 13:36, 18 November 2024

for ordinary differential equations are methods used to find numerical approximations to the solutions of ordinary differential equations (ODEs). Their...

28 KB (3,919 words) - 15:32, 12 June 2024

Euler–Maruyama method (category Stochastic differential equations)

of a stochastic differential equation (SDE). It is an extension of the Euler method for ordinary differential equations to stochastic differential equations...

6 KB (827 words) - 17:13, 5 August 2024

backward stochastic differential equation method is a numerical method that combines deep learning with Backward stochastic differential equation (BSDE)...

181 KB (17,903 words) - 03:58, 21 November 2024

particular, the theory of stochastic processes. He invented the concept of stochastic integral and stochastic differential equation, and is known as the founder...

19 KB (1,702 words) - 00:19, 23 November 2024

differential equation Cauchy–Euler equation Riccati equation Hill differential equation Gauss–Codazzi equations Chandrasekhar's white dwarf equation Lane-Emden...

13 KB (1,095 words) - 23:44, 15 November 2024

backward stochastic differential equation method is a numerical method that combines deep learning with Backward stochastic differential equation (BSDE)...

28 KB (4,110 words) - 17:20, 28 September 2024

Milstein method (category Stochastic differential equations)

of a stochastic differential equation. It is named after Grigori N. Milstein who first published it in 1974. Consider the autonomous Itō stochastic differential...

6 KB (1,131 words) - 22:48, 4 August 2024

Physics-informed neural networks (category Differential equations)

backward stochastic differential equation method is a numerical method that combines deep learning with Backward stochastic differential equation (BSDE)...

34 KB (4,421 words) - 16:28, 23 November 2024

Rough path (category Differential equations)

case, the aforementioned controlled differential equation can be interpreted as a stochastic differential equation and integration against " d X t j {\displaystyle...

29 KB (5,731 words) - 06:28, 12 July 2024